The “ceasefire” in eastern Ukraine is still very precarious, but at some point we may see a stabilization of the military standoff, after which the crisis in Ukraine will likely enter a new phase in which economic war replaces actual war as the main instrument of contestation. If so, we are very likely to witness a costly and prolonged game of beggar-thy-neighbor economic policies between Russia and the West. In my previous post, I argued that the Russian economy is in serious trouble, and that in the long run Russia is unlikely to win this game. But the game is going to be painful for all parties – first and foremost for Ukraine, but also for Western Europe and even, to a limited extent, the United States.

The intent of this post is to put Russia’s economic difficulties in perspective by focusing on the economic fallout from the crisis for Ukraine, Western Europe, and the United States. I will also consider the political consequences of that fallout.

Ukraine’s economic crisis

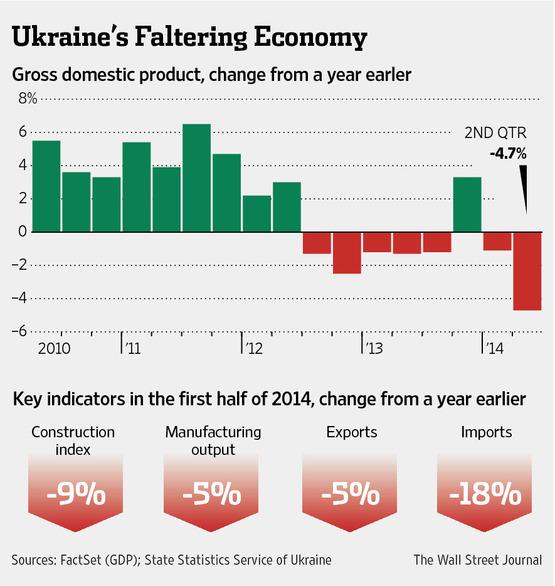

By any measure, Ukraine’s economy is in dire shape. In its September 2 report on the status of its Stand-By Agreement with Ukraine, the IMF estimated that Ukraine’s GDP would contract by 6.5% in 2014 and grow by a meager 1.0% in 2015. It added, however, that a prolonged conflict in the Donbas would cause GDP to decline by 7.25% in 2014 and 4.25% in 2015.

Stand-By Agreement with Ukraine, the IMF estimated that Ukraine’s GDP would contract by 6.5% in 2014 and grow by a meager 1.0% in 2015. It added, however, that a prolonged conflict in the Donbas would cause GDP to decline by 7.25% in 2014 and 4.25% in 2015.

Inflation in Ukraine is also accelerating. A forecast this month by FocusEconomics has Ukrainian inflation for 2014 at 17.1% and 7.2% next year. Manufacturing, which is concentrated in the east and south of the country and has been particularly disrupted by the violence in the Donbas, is down some 20% this year. Total exports are down some 20%. The Ukrainian currency, the hryvnia, is in free fall, having declined from five to the dollar last year to 14.5 to the dollar last week.

Source: The Economist

Meanwhile, Ukraine is on financial life support by the international community. In September, the IMF released a second tranche of the $17.1 billion loan agreed to in April, which brought total disbursements to date to $4.51 billion. But it indicated that it had underestimated the extent of the country’s financial needs and that Ukraine was going to need an additional $19 billion by the end of 2015, summarizing the country’s economic condition as follows:

Notwithstanding a more favorable current account deficit path, the balance of payments is weaker than projected at the time of the program request-–by over US$7.5 billion in 2014 and US$11.5 billion in 2015—reflecting reduced FDI, higher outflows from the banking system, much lower liability rollover rates for banks and corporates (and no external market access for the sovereign), and substantial capital flight. Meeting these external pressures while maintaining the programmed central bank gross international reserves would require an additional external financing of about US$19 billion by end-2015 relative to the baseline.

Source: The Economist

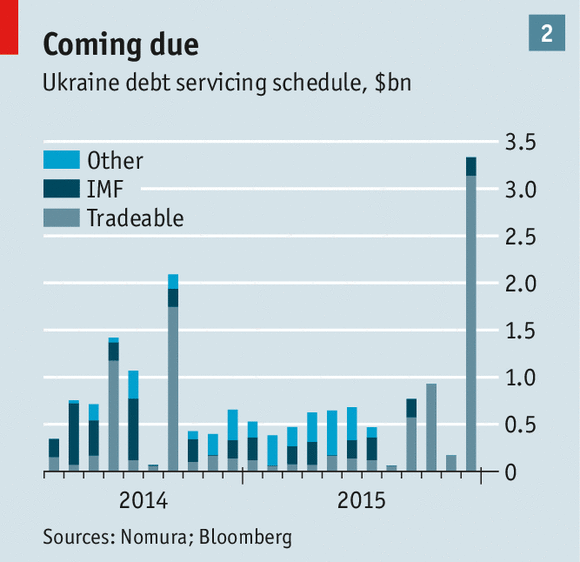

This was written before an 11% decline of the hryvnia on September 19. That same day, yields on Kyiv’s sovereign debt rose 155 basis point, bringing yields on five-year Ukrainian bonds to around 11.5%. Ratings agencies characterize Ukraine’s sovereign debt as “highly speculative,” just above “in default, with no prospect for recovery.”

In short, if Kyiv does not get more financial assistance from the international community, it will be forced to default at some point in the coming months. If the war in the east reignites, or if Russia invades openly, its financial needs will only get worse. The problem, however, is that the IMF is not supposed to lend money to countries in financial distress unless they have a reasonable prospect of paying those loans back. As a result, Ukraine has probably already reached the point where IMF loans will be forthcoming only if they are guaranteed by Brussels or Washington.

Particularly important politically is Kyiv’s $4.5 billion debt to Gazprom. Last week, Kyiv agreed to pay $3.1 billion of the debt this year. In exchange, Gazprom reportedly agreed to resume gas deliveries over the winter, although there is apparently still a dispute over the price. The European Union has nevertheless indicated that it will guarantee an IMF loan to cover part of the payments. The implication is that future IMF loans are likewise going to put voters in the EU or the U.S. on the hook, and that in effect Western taxpayers are going to be asked to subsidize Ukrainian gas imports from Russia at what may prove to be above market prices.

Western efforts to prevent Ukrainian default on its sovereign debt may become even more difficult in the coming months if financially vulnerable governments like Ukraine’s experience a spike in borrowing costs as investors move short-term investments to the United States in anticipation of rising U.S. interest rates. The Fed is widely expected to begin a long, albeit gradual, increase in interest rates in the summer or fall of 2015. If the flow of money chasing US bond yields becomes a flood, countries like Ukraine are going to be in even bigger trouble.

To be sure, there is a silver lining in the loss of control over the Donbas for Kyiv that warrants mention. Before the uprisings, the east accounted for some 15% of Ukraine’s GDP and 25% of its exports. These figures are, however, somewhat misleading, because the region’s heavy industries were heavily, if indirectly, subsidized by the low cost of gas imported from Russia. At market prices for energy, those industries were not going to be competitive, which made both reducing government energy subsidies as well as integration with Europe more difficult.

Moreover, while a Novorossiya beyond Kyiv’s writ means that tax revenues and export duties from the breakaway republic are going to be lost to Kyiv, it is also true that Ukraine’s eastern regions took in more from the central budget than they provided in revenue before the crisis. Kyiv is also not going to have to keep the region’s uncompetitive industries afloat, pay for the reconstruction of the region’s devastated infrastructure, or provide social services, including pensions, to civilians in the region.

Moreover, while a Novorossiya beyond Kyiv’s writ means that tax revenues and export duties from the breakaway republic are going to be lost to Kyiv, it is also true that Ukraine’s eastern regions took in more from the central budget than they provided in revenue before the crisis. Kyiv is also not going to have to keep the region’s uncompetitive industries afloat, pay for the reconstruction of the region’s devastated infrastructure, or provide social services, including pensions, to civilians in the region.

Nevertheless, the strategic problem for the West is that it is going to be much less costly for Russia to undermine its neighbor economically than it will be for the West to prop it up. Russia continues to have a great deal of military, political, and economic leverage over the country, including natural gas supplies. Gradually, Ukraine’s vulnerability to Russian economic pressure may diminish, but that will take time. In the meantime, the country can count on very troubled economic waters ahead, and the West can assume that calming those waters is going to prove very costly.

The economic travails of the European Union

If the Ukrainian economy is in crisis, the EU economy is in serious trouble. It is perhaps no exaggeration to assert that the fate of the EU – and the European project broadly – is going to be determined by whether its economy can recover fast enough, and vigorously enough, to stem the rising tide of Europe’s far-right and far-left anti-system parties.

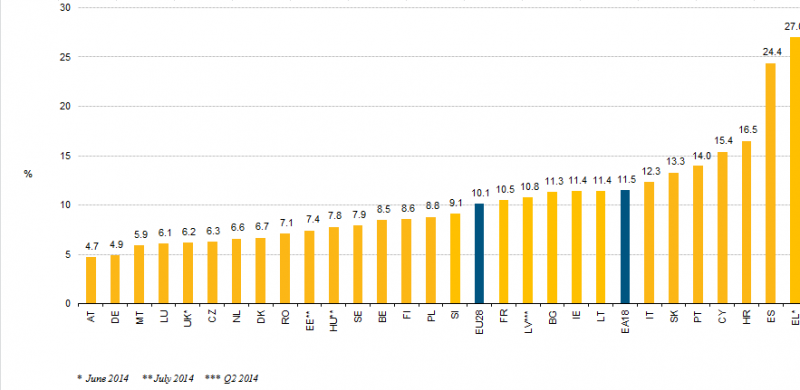

Unemployment in Europe by country (Source: Eurostat)

Since the end of the Great Recession, average annual growth for the EU has been a paltry 0.8% – meaning five years of stagnation. In the Eurozone countries, there has been a net contraction – output has yet to recover to where it was prior to the recession. According to Eurostat, EU-wide unemployment in August was 10.1%; in the Eurozone, the rate was 11.5%. In Greece and Spain, unemployment was 27% and 24% respectively (see chart). By way of comparison, unemployment in the EU (EU-28) and Eurozone (EA-18) is much higher than it is in the US, and it has declined much less since the end of the Great Recession in 2009 (see chart below).

Unemployment rates EU-28, Eurozone 18, US and Japan (Source: Eurostat)

Earlier this year, there were signs that growth in Europe was finally starting to pick up. The European Commission forecast growth for the EU at 1.5% for 2014 and 2.0% for 2015. Eurozone growth was predicted to come in at 1.2% in 2014 and 1.8% in 2015. The sense of optimism has since subsided, particularly for the Eurozone, which recorded essentially zero growth in the second and third quarters this year. (Non-Eurozone growth is being helped by the U.K., which the IMF expects to grow 3.2% this year and 2.7% in 2015). The Economist Intelligence Unit has since lowered its forecast for growth in the Eurozone to 0.8% for 2014 and 1.2% in 2015.

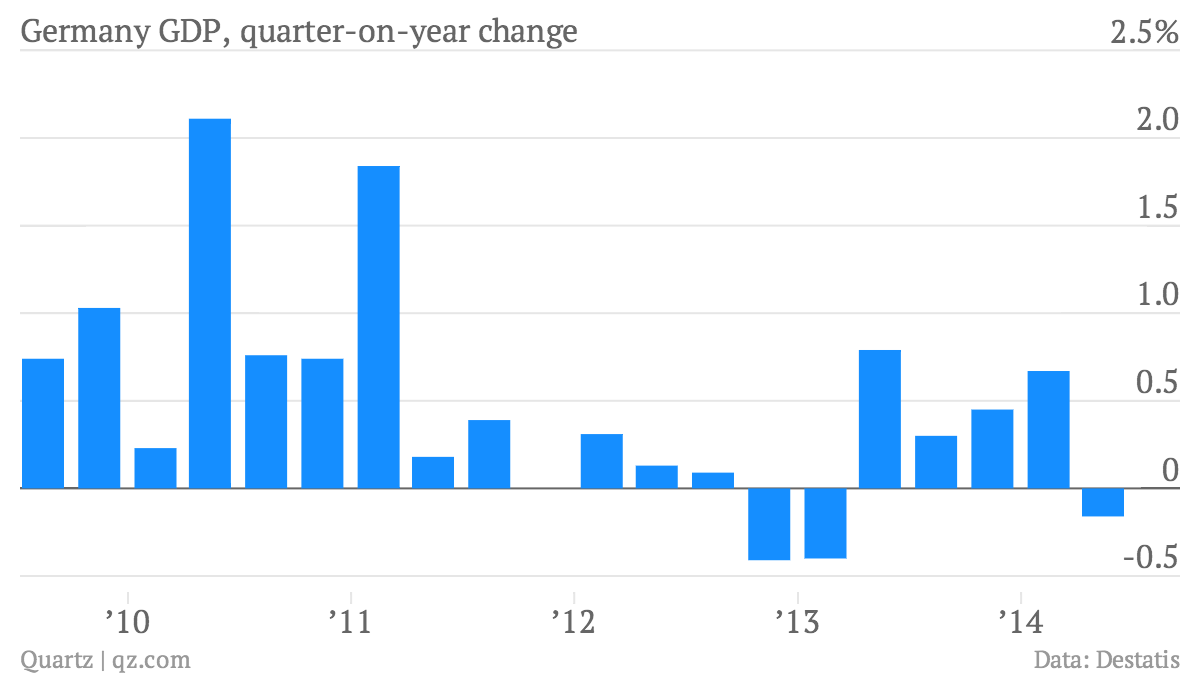

Particularly worrisome is the health of the German economy, which may now be in recession after contracting 0.2% in the second quarter. The German economy’s resilience has kept the EU, and particularly the Eurozone, from doing even worse over the past five years. A prolonged German slowdown is going to make other major European economies – France, Italy, and Spain, all of which depend on Germany for trade and investment – even more stressed.

Particularly worrisome is the health of the German economy, which may now be in recession after contracting 0.2% in the second quarter. The German economy’s resilience has kept the EU, and particularly the Eurozone, from doing even worse over the past five years. A prolonged German slowdown is going to make other major European economies – France, Italy, and Spain, all of which depend on Germany for trade and investment – even more stressed.

More broadly, the European Central Bank (ECB) is struggling to avoid deflation, which the great bulk of economists consider a much more difficult problem to overcome than inflation. In the 12 months ending in August, inflation in the Eurozone was 0.3%, well below the ECB’s target rate of 2%. The ECB’s president, Mario Draghi, recently announced another cut in interest rates, along with a new quantitative easing-type stimulus program. There are, however, significant legal and political obstacles to the kinds of unconventional monetary policies that the US Federal Reserve has pursued in recent years. As for interest rates, a key bank deposit rate is now -0.2%, which means that the ECB is in effect punishing banks that hold onto cash rather than lending it. The ECB is also encouraging a fall in the Euro against the dollar in an effort to promote exports and increase prices. In noting these efforts, The Economist commented that “we do believe that these measures will have a transformative effect.”

Europe, in short, has a growth crisis. The causes of this crisis are mostly internal and include institutional factors (economic decision-making constraints from unanimity or qualified-majority voting rules, monetary union with national fiscal autonomy, rules constraining the ECB from engaging in quantitative easing); policy-related factors (monetary and fiscal austerity despite weak aggregate demand, an unwillingness of national governments to undertake supply-side reforms, an unwillingness of national governments to borrow at currently low rates to improve infrastructure); and cultural factors (weak sentiments of solidarity across national publics).

There are, however, important external factors as well, including general weakness in the global economy. The EIU expects global growth to be 2.4% in 2014 and 3.0% in 2015, which compares to an average rate of 3.8% over the past five decades. But it is also true that one of these external factors – and one that is likely to have important political consequences – is the sanctioning of Russia for its role in the Ukraine crisis.

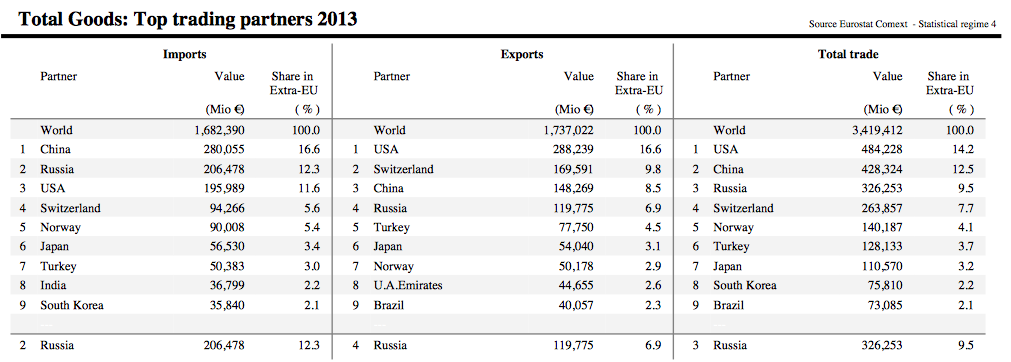

Over the past decade, Russia has become an important trading partner for the EU. In 2013, 12.3% of total EU imports came from Russia, while 6.9% of EU exports went to Russia. The EU also accounted for some 75% of total foreign direct investment in Russia. Pimco recently summarized the economic fallout from the Ukraine crisis on the EU as follows:

Over the past decade, Russia has become an important trading partner for the EU. In 2013, 12.3% of total EU imports came from Russia, while 6.9% of EU exports went to Russia. The EU also accounted for some 75% of total foreign direct investment in Russia. Pimco recently summarized the economic fallout from the Ukraine crisis on the EU as follows:

Geopolitical tensions from Ukraine threaten what is already a weak recovery in its neighbouring European economy. The situation is very fluid and things can change rapidly, but – as things stand – we think that the crisis will shave approximately 0.3% off eurozone GDP. This is a modest impact overall, but one that will be felt in an environment of already-very-low growth. And things could be worse: If tensions in Ukraine escalate, the eurozone could plunge back into recession.

Germany in particular has extensive economic interests in Russia. Russia was export-oriented Germany’s 11th largest trading partner, and as many as 300,000 German jobs are said to depend on Russian-German trade. Some 6,200 German firms do business there, and German individuals and business have around $25 billion invested in Russia. Germany’s exports to Russia may fall by as much as 20-25% this year. Little wonder, then, that Germany’s business community has been particularly vocal in opposing sanctions on Russian.

Again, then, there is the question of how the blame game plays out, and again the key country is Germany, which is now the most important driver of EU economic and foreign policy. In late August, the German Finance Ministry asserted that Germany’s second quarter contraction was “likely to have been related to the effect of sanctions and negative effects on confidence due to the Ukraine crisis,” an interpretation that is clearly shared by many in Germany’s business and financial community. Gerhard Schroeder, the former chancellor and now chairman of the board of Nord Stream AG (which constructed and now operates the gas pipeline delivering Russian gas to Germany under the Baltic Sea) put the argument bluntly in a speech this week: “The mutual sanctions are causing immense damage to both sides. Politicians in Russia and Europe must find a way out of the spiral of ever tougher sanctions… Germany doesn’t need a new Russia policy based on confrontation, as is being demanded by some hawks.”

While sanctions may have precipitated Germany’s second-quarter contraction, Germany’s low rate of trend growth almost certainly has deeper, structural causes (see “Germany’s Economy: Three Illusions,” in the latest issue of The Economist). However, structural problems by definition are either economically or politically costly to address, and it is accordingly less painful for elites and publics to blame external or superficial factors for economic problems. In the German case, there are two principle alternatives to blaming domestic structural factors – the Euro (and less clearly, at least in Germany if not elsewhere in Europe, the EU) on the one hand, and sanctions on Russia on the other hand.

While sanctions may have precipitated Germany’s second-quarter contraction, Germany’s low rate of trend growth almost certainly has deeper, structural causes (see “Germany’s Economy: Three Illusions,” in the latest issue of The Economist). However, structural problems by definition are either economically or politically costly to address, and it is accordingly less painful for elites and publics to blame external or superficial factors for economic problems. In the German case, there are two principle alternatives to blaming domestic structural factors – the Euro (and less clearly, at least in Germany if not elsewhere in Europe, the EU) on the one hand, and sanctions on Russia on the other hand.

The rapid rise and political successes of the new Alternative for Germany party – which when it formed last year had only one clear demand, which was to abandon the Euro – suggests that the “blame the Euro” argument is gaining strength even in Germany. It also suggests that the still very popular Angela Merkel may become politically vulnerable if the German economy continues to underperform. But an extended slowdown in Germany will also very likely make the German public less supportive of sanctions as well.

The Alternative Party has yet to decide if it will fall into line with many other right-wing parties in Europe and announce its opposition to sanctions. It may well decide against doing so, given that polls in Germany show a dramatic shift in public opinion about Russia after the downing of Malaysian Airliner Flight MH-17. A survey taken in early August indicated that 82% of Germans felt that Russia could not be trusted and 70% supported tougher sanctions. But it is far from clear how long that support will last. And again much depends on how the German economy performs going forward. Earlier this week, Merkel stated that the EU is still “very far away” from lifting sanctions on Russia. But left unsaid was just “how far?” The answer may be “not that far” if the German economy does not start to pick up soon, if the Alternative Party replaces the liberal Free Democrats as a needed coalition partner for the CDU, if the business community continues to lobby for economic rapprochement with Russia, or if surveys show German public opinion shifting against sanctions.

Source: The Economist

And there are of course other increasingly influential anti-EU parties across Europe, many of which are pro-Russian (the UKIP in Britain being a notable exception). They, too, are likely to grow in strength if European economies continue to struggle. France in particular, the other key driver of post-war European unity along with Germany, may experience a political upheaval thanks to low growth, high unemployment, and mounting fiscal pressures. In a report earlier this week, Stratfor summarized France’s problems as follows:

External pressure from the European core pushes for a reduction of spending and a balancing of the books, while the French public, the labor unions and a large proportion of the sitting parliament support the 35-hour work week, a tax-and-spend outlook, and the “war on finance” that Hollande promised in his election campaign. Caught in the middle is a president facing the lowest approval rating of any president in the Fifth Republic and suffering a year of scandal in his private life, whose prime minister has also seen a collapse in popularity since May. The elephant in the room is the National Front of Marine Le Pen, a right wing anti-immigration party that has been gathering momentum. Indeed, a recent poll revealed that Le Pen would defeat Hollande in a run-off were the presidential election to be held immediately. But the likeliest benefactor of Hollande’s weakness is former President Nicolas Sarkozy, who declared his return to politics in September and seems certain to be a strong presidential candidate in 2017.

In short, the political fallout from Europe’s economic travails means that Moscow can reasonably expect public support for sanctions in Europe to decline in the coming months and years. While the results of the Scottish independence referendum were a disappointment for the Kremlin, Moscow can also hope, again with good cause, that Le Pen will win the French presidency in 2017; that David Cameron will be reelected British prime minister and Britain will vote to leave the EU in Cameron’s promised referendum; that separatists in Catalonia continue to press ahead with their independence project; and that pro-Russian populist parties will become increasingly influential in European capitals and in Brussels. At the least, Moscow can expect the EU economy to struggle for at least the next several years, trend growth in the EU to be 2% or lower for the foreseeable future, and economic difficulties to widen political divisions within Europe and keep EU foreign and security policy weak and disjointed.

The United States

Of the major parties involved in the geopolitical contest over Ukraine’s external orientation, the one that is least vulnerable to negative economic fallout is the United States. Total US trade with Russia made up less than 0.1% of U.S. GDP in 2013. U.S. investment exposure in Russia is minimal – less than 0.5% of total U.S. overseas investment, and 1.1% of overseas loans by U.S. banks. U.S. economic involvement in Ukraine is even more limited.

From “Conversable Economics” blog

The US economy also appears to be finally picking up steam after years of slow growth since the end of the Great Recession. After a difficult first quarter, during which the US economy shrank by 2.1%, U.S. GDP rose by 4.6% in the second quarter. Unemployment has fallen to 5.9%, down from a post-recession peak just over 10%. The economy is expected to grow at an annualized rate of around 3% for the remainder of the year, and most forecasters are predicting growth of around 3.0% to 3.2% in 2015 and slightly higher for 2016.

While the post-Great Recession recovery has been long and painful, the long slog was broadly predicted by mainstream economists who argued that major financial crises are typically followed by slow and intermittent recoveries. (See, for example, Carmen M. Reinhart and Kenneth Rogoff, This Time Is Different: Eight Centuries of Financial Folly). My view is that the U.S. has been very fortunate that it has had accommodative macroeconmic policies, particularly monetary policy, since late 2008. I also believe that bad macroeconomic policies were much more likely politically than better ones, which is to say the recession could have been much worse.

The important point, however, is that the U.S. is recovering considerably faster than the E.U., as shown in the chart below. Investors are also signaling that they expect growth in the U.S. to exceed that of Europe, and much of the rest of world, for at least the next several years. As an article last week in The New York Times explained:

The United States dollar has now re-emerged as the preferred currency for global investors…. It has gained about 3.2 percent against the euro since Aug. 20, and about 8 percent against the yen since July 1. The rise underscores expectations that the United States economy will continue to grow at a faster clip than that of Europe, Japan and even large emerging markets, all of which are seeing their economies stagnate… Still, the increasing push by investors into the dollar can be seen as a favorable report card on the United States economy, highlighting good performance in crucial benchmarks such as growth and fiscal responsibility, and an increasingly competitive position abroad because of a boom in energy exports.

Of course, the U.S. has serious economic problems other than low growth, including comparatively high and growing inequality, stagnant or declining median income, low overall employment, high national debt by post-World War II standards, and unfunded entitlement obligations over the long term. Robust growth would, however, go a long way toward solving at least some of those problems, notably national debt and entitlement funding. It would also be a very helpful lubricant for addressing the others, although it would not by itself reduce inequality or raise middle class incomes. Still, growth of 3% or more for the next two years would be enormously helpful to the Obama Administration, especially if it meant a meaningful rise in middle class incomes. It would also make it much more likely that a Democrat succeeds Obama as president, and that the Democrats otherwise do well at the ballot box in 2016.

The main economic challenge – and indirectly the main geopolitical challenge – for the U.S., then, is unlikely to be economic performance over the next two or three years. Rather, it is the possibility of low trend growth over the longer term. If arguments about “secular stagnation” in the U.S. are correct, then the U.S. is entering into a long period of low growth by historical standards – say 2% rather than 3.0 to 3.3% (see, for example, the argument in Lawrence H. Summers, “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bond”). Secular stagnation, I have no doubt, will make the U.S. increasingly difficult to govern. It will also make it all the more difficult to address the country’s other economic problems, notably income and wealth inequality.

Of course, it may turn out that trend growth in the U.S. holds up just fine. The energy revolution from fracking and from increasingly competitive alternative fuels is lowering manufacturing costs and making the U.S. increasingly less dependent on imported oil. It is also a reminder that growth in a market economy is a discovery process – that is, it is very difficult, if not impossible, to predict where innovation will lead to unexpected “creative destruction” and new growth opportunities.

Even if the U.S. returns to its historical pattern of robust and dynamic growth, the United States is still facing an increasingly hostile and dangerous international environment. The Obama administration has, rightly in my view, focused its political attention on domestic problems, particularly the economy. But the Middle East is a complete mess, the international jihadist movement has never been stronger, and the United States is confronted with two powerful illiberal states in China and Russia, both of which feel the rules of the international game have been stacked against them, and both of which have powerful militaries that can prevail in a conflict along their borders.

Conclusions

The title of this post – “Ukraine and the War of Recessions” – is admittedly slightly misleading. Of the four main parties in the conflict – the U.S., the E.U., Russia, and Ukraine – only Ukraine is clearly in recession at the moment. The U.S economy is picking up, and although it is not yet at full employment, it is getting there. But the political effects of the Great Recession are still very much with us. And Russia and the E.U. are growing very slowly, if at all, and it may turn out that Russia and the Eurozone are technically in, or about to enter into, a recession.

Indeed, one way to think about how the Ukraine crisis will play out politically is to treat it as a competitive game involving objective economic costs, subjective economic pain thresholds, and blame assessment.

In Ukraine, objective economic pain is severe and worsening. Politically, the key question is whether the public will conclude that economic contraction is an acceptable consequence of defending the country against separatists and Russian aggression. If not, Ukrainians will have to decide whether to place primary blame for deepening hardships on Poroshenko, the government, the political class as a whole, the oligarchs, the IMF, the E.U., the United States, or Russia.

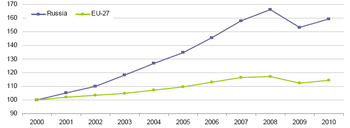

GDP growth index (2000=100): Why Putin has more political capital (for now) than the leaders of EU member-states

In Russia, the public’s tolerance for pain may turn out to be high, thereby allowing Putin to continue to benefit from having annexed Crimea and shown the world that Russia still matters. On the other hand, a prolonged slump may well lead the electorate to blame, sooner or later, Putin and his policies for declining living standards, growing uncertainty, and the permanent hostility of Russia’s most important Slavic neighbor. Indeed Putin may well discover that an unfortunate consequence of concentrated political power is concentrated blame when things go wrong.

Europe has been in a slump since 2008, and some European countries have experienced a contraction every bit as bad as that in the U.S. during the Great Depression. There can be no doubt that the pain threshold has already been breached. The question is whether electorates place most of the blame on national governments, internal structural rigidities, the Euro, the EU, or sanctions for the Union’s economic difficulties.

As for the United States, its economy is finally recovering, and it is once again likely to be a major contributor to global growth over the next several years. Its very limited economic ties to Russia gives it more freedom of action than Europe in responding to the Ukraine crisis, and its dominance of international finance, particularly its influence over the SWIFT system for international banking transactions, gives it considerable economic leverage over Russia. But it is also facing a host of intractable and costly challenges around the globe, and it is in no position to take the kinds of steps to defend NATO’s eastern borders that the United States took during the Cold War.

Let me conclude with my brief take on how the economic fallout from the Ukraine crisis is likely to play out politically. In Ukraine, I suspect most of the blame will eventually fall on Russia’s shoulders, but in the short term the country is in for a period of political turmoil, thanks in part to economic factors but also to Ukraine’s losses on the battlefield.

In Russia, the economic pain threshold is likely to prove relatively high, which means that it will take several years at least before economic stress starts to put serious pressure on Putin’s popularity. But I think eventually Putin will not prove immune to the general rule that prolonged economic stress makes for unpopular leaders.

As for Europe, the Eurozone is suffering from a severe liquidity trap that may well get worse — at the least, it will mean prolonged economic weakness and at worst a genuine depression. As a result, unless Russia decides to invade Ukraine outright, I suspect that public support in Europe for sanctions and for a robust military response to Russia’s actions in Ukraine is going to gradually abate.

In the United States, public attention is focused on the turmoil in the Middle East, and after more than a decade of costly and unsuccessful wars in Afghanistan and the Middle East, there is little public appetite for spending a great deal of money trying to bolster NATO’s eastern defenses. As a result, I expect that the Obama administration will eventually look for ways to reduce tensions with Moscow.

To sum up, all parties have a considerable economic and political interest in de-escalation, above all in the military arena. Militaries are expensive, wars even more so. If the violence does not spread, realists on all sides at some point – perhaps this winter, perhaps next year, perhaps later – will likely come to the conclusion that it is better to talk than fight, and they will seek to negotiate an arrangement that makes an extremely dangerous military relationship less dangerous and a very costly tit-for-tat economic war less costly.